Important Accounting Terms for the Non-Accountant

Depreciation

We use this method to allocate the costs of a large purchase over the useful life of the purchase. Let’s look at it using an example:

- You purchased a new van for $25,000 and placed it into service on the first day of the year. The purchase is recorded as a new fixed asset.

- Using an IRS-approved depreciation method at the end of the year, your accountant will record a portion of the van’s value as an expense. This will decrease your tax liability.

- Accumulated depreciation will always carry a negative balance on your balance sheet because it reduces the value of an asset. Suppose we want to know the value of an asset that has been depreciated. In that case, we take this value from the net of the asset account and the accumulation account.

Debits and Credits

I’ve always used the DEALER acronym, where each letter corresponds with one of the different types of accounts in your books:

- Dividends

- Expenses

- Assets

- Liabilities

- Equity

- Revenue

Debits are on the left in a journal entry, and credits are on the right. A debit will increase asset and expense accounts, while a credit will increase liability and equity accounts. The reverse is also true. Debits decrease assets and expenses, while credits decrease liabilities and equity.

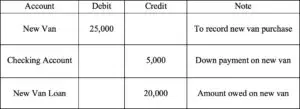

- Example: Let’s record the purchase of the new van we discussed earlier. We put down $5,000 and financed the rest:

- Now we have a new van at a value of $25,000, we’ve spent $5,000 on the down payment, and we still owe $20,000. All of this information is from a simple entry!

Accounts Payable

Quite simply, accounts payable includes any unpaid amounts owed to vendors and suppliers. As you’re still liable for payment, A/P should be classified as a liability. When we record accounts payable, we utilize the double-entry system to record the A/P and expense simultaneously.

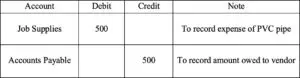

- Let’s look at an example where we purchase some PVC pipe on account:

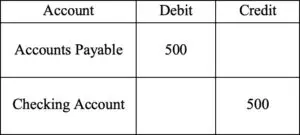

- When it’s time to pay our vendor, instead of recording the expense, we’ll reduce Accounts Payable, which will also reduce cash in this case:

Job Costing

You’ll incur certain costs no matter how busy you are. Typically these are referred to as indirect or overhead costs since we can’t tie them back to a particular job.

Other costs, though, are only incurred once you begin a job. For instance, every job you perform requires a different amount of materials – and time!

For instance, take your payroll, for example. Your receptionist does a lot for you around the office, and her labor can’t be tied to a particular source of income. Her wages would be considered an indirect or overhead expense.

Your field technician, however, works on a job-by-job basis. Therefore, their time working on these jobs could be considered direct labor.

Tracking direct expenses on a job-by-job basis is a simple definition of job costing. Job costing can often be the key to understanding where your margins are strongest and where they can use improvement.

S-Corp

Who wants to pay taxes twice? Unfortunately, this is the case year after year for some sole proprietors and partnerships. For these entities, anything paid to the owners outside of payroll passes through to the owner as personal income. Therefore, besides paying income tax, these owners will also be required to pay a self-employment tax of 15.3% on the first $142,800 of their earnings.

Electing to be taxed as an S-corporation provides alleviation of this double taxation. Once you make an S-corp election, the owner’s pay outside of payroll is no longer subject to self-employment tax.

In order to maintain the S-corp status, a few key items must be true:

- You must pay yourself a reasonable salary through payroll

- Shareholders of an S-corp cannot be another corporation

- Shareholders must be citizens or resident aliens of the USA

- You must have a written operating agreement

- Consult the IRS website for an all-encompassing list

Balance Sheet

The balance sheet tells you three important things.

- What do we have?

- Traditionally, the balance sheet will list assets first. Assets are the items of value that your business owns. This includes things like cash, vehicles, and inventory. Accounts Receivable is also considered an asset because we assume it will be converted into cash.

- What do we owe?

- The second section on the balance sheet deals with liabilities. These include short-term liabilities like Accounts Payable and long-term liabilities like vehicle loans.

- What’s leftover?

- Last on the balance sheet, but certainly not least, is the equity section. The simplest definition of equity is the difference between assets and liabilities recorded on the balance sheet. For instance, if you have assets of $50,000 and liabilities of $30,000, you have $20,000 in equity in your business. The reverse can also be true – if you owe more than you have, this is considered negative equity.

Profit and Loss

The Profit and Loss points out three key indicators.

- What did we make this period?

- The first section of the P&L deals with income. The breakdown of your income should be as detailed as possible so you can identify where your income is coming from.

- What did we spend this period?

- Cash outflows are typically classified as one of two things – Cost of Goods Sold or Expense.

- Cost of Goods Sold is cash outflows that can be traced to a specific job.

- Expenses are costs incurred that are necessary for the operation of the business but can’t be traced to a specific job.

- Cash outflows are typically classified as one of two things – Cost of Goods Sold or Expense.

- What’s leftover?

- After all is said and done, this report’s last piece of information is arguably the most important. Listed as the last line item on the report, the net income of a business is often appropriately referred to as “the bottom line.” This number is simply the difference between income and expenses for the period.

Ready to find out more?

Drop us a line today for a free quote!