How To Make A Chart Of Account Specific to Contractors?

One of the most critical aspects of your accounting and bookkeeping is your chart of accounts. It is the backbone of your financials because it determines your statements and taxes. When designing your chart of accounts, you must keep the IRS requirements in mind as well as your own businesses’ needs.

There are six main account types: assets, liabilities, equity, income, cost of goods sold, and expense accounts. Even the most basic chart of accounts should include most of these items. Income and expenses are required for a profit and loss, while assets, liabilities, and equity make up the balance sheet. Keep in mind that every business will have its own needs and breakdown, but we see some industry-wide trends when doing bookkeeping.

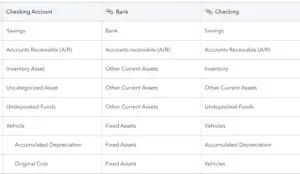

Assets

Of course, when thinking about asset accounts, bank accounts and cash are the first things that come to mind. For example, undeposited funds and accounts receivable are required current assets in QuickBooks. Accounts receivable tracks payments owed, while undeposited funds track payments received but not yet deposited to the bank. Accounting software like QuickBooks may also have accounts that they require, such as uncategorized assets. We recommend not using this account despite it existing in the premade CoA.

When considering contractor-specific assets, the leading fixed asset we see are vehicles. These are important to record accurately because there are a lot of parts to recording a vehicle on your books. This means having an account on the CoA for each vehicle to better track value if the owner decides the company will be sold in the future. We would also recommend breaking out depreciation individually for more accessible tax valuation, as shown below in the asset example.

Another important asset that many contractors use is inventory, accounting for the supplies kept on hand in either the warehouse or trucks. Finally, the last most common contractor fixed asset is buildings. It is becoming more common for businesses to buy their warehouses rather than lease or rent them.

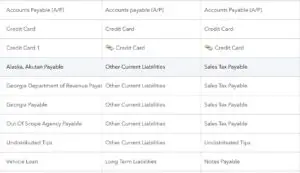

Liabilities

Common current liabilities are credit cards, sales tax payable, and accounts payable. Sales tax payable is a running total of your sales tax owed to the state. Accounts payable is an excellent tool for contractors who use large distributors, like Ferguson, who send multiple invoices to be paid at once. A/P allows for the cost of goods sold or expense accounts to accurately depict their values at any given time. Finally, an undistributed tips account is a more uncommon current liability that contractors may find beneficial. This liability is where tip payments go when received but are not yet paid out to the recipient.

Building loans, vehicle loans, and any other loans that will be paid off in over a year should be considered a long-term debt account type.

Payroll liabilities are a set of accounts that are highly tailored to the company. These amounts are taken from the employees’ paycheck and held in liability until paid out to the correct agency. A simple example is below, but adding different benefits can quickly complicate the payroll liabilities.

Equity

The least well-known piece of the chart of accounts is equity. Equity accounts include the four main accounts for all companies. Owner’s draws or distributions, owner’s contributions, opening balance equity, and retained earnings. The owner’s draws and contributions are what the owner has taken out of the company and invested into the company, respectively.

Opening balance equity is the account that is used to offset any opening account balances from the previous software. Finally, retained earnings are QuickBooks’ automatic chart of accounts that rolls over net income every year. It is a lifetime net income or loss of the company. That was a quick summary of the balance sheet accounts that we see used by contractors across the board.

The chart of accounts that make up the profit and loss statement is where the customization comes alive. Income, costs of goods sold, and expenses define a company and track within the operations.

Income and Cost of Goods Sold

Sales and services should not just break down income because income can track more information based on your industry. For example, if your services include install and maintenance, having the income reflect those two different revenue streams will give you a better idea of which stream is grossing more revenue. Therefore, when setting up your income accounts, the most important thing is creating them based on your industry and your specific business to account for your actual revenue streams.

First, if you are not using inventory, there is no cost of goods sold per the IRS. However, the cost of goods sold accounts is imperative for advising and budgeting. Your cost of goods sold accounts should mirror your income accounts because it allows for comparing each revenue stream to the direct costs associated with the jobs.

Comparing the income accounts to the cost of goods sold accounts tells the business a better picture of their gross profit, whether their prices are making up for expenses, and where to focus efforts to grow a division.

Expenses

Below you can see the general expenses for our client’s chart of accounts. Some of the names are ones or very similar to what Quickbooks auto-generates in their chart of accounts. Many of these accounts are also created because they are items the IRS wants to be broken down specifically.

It comes down to what is essential for you to see beyond those requirements for your business. Examples include:

- If you believe your advertising is too high or want to track where your money is going, having a breakdown of physical, digital, and lead advertising would be beneficial for you.

- Insurance: Not everyone has the same insurance type for your industry, so you will want to customize this section for what is covered.

Job Supplies can be broken down the same way as the cost of goods sold. For example, if you buy parts for installations only, but those parts will be used for multiple jobs, you will categorize these expenses to job supplies.

In the end, this is another reason why having a contractor-specific accounting team is essential for your business. The ability to structure your chart of accounts to show you what the IRS needs, your industry needs, and your specific business needs is crucial to understanding and adapting your business practices to be successful

Ready to learn more?

Whats Up Next?