What are Journal Entries and how to use them correctly?

A Journal Entry is a way to record a business transaction in accounting. Think of it like writing in your notebook about your day – but instead of doing that, you’re recording the money coming in and going out of an account/business. The key parts of a journal entry are the date, the amounts, the description, and the accounts involved.

We will discuss what it looks like and how to use them appropriately as we progress. By the end of this blog, you will have an in-depth understanding of the answers to the title of this blog and a little additional information.

How do I use them? What do I need to know before using them?

A journal entry is the basis of all accounting, and it helps businesses keep track of every transaction so their financial records stay accurate. Fortunately for us in the modern technology world, we have tools accessible to us, such as Xero, Sage, and our preferred software, Quickbooks, and there are others out there that are not named.

Most of the time, this software helps with behind-the-scenes journal entries instead of manually entering them. From this point on, we will focus more specifically on the benefits of Quickbooks; likewise, this can be applied across different systems.

Firstly, remember that before creating journal entries, it’s essential to build a General Ledger (G/L), also known as Chart of Accounts (COA), used in Quickbooks. A G/L or COA is the main record of a business’s financial transactions. It’s where all the journal entries are organized, sorted, and grouped by account.

Think of it like this: journal entries are daily notes of what’s happening financially, and the G/L or COA is the whole story, organized by topic (account). The G/L (COA) is used to prepare financial statements such as the income statement (Profit & loss) and balance sheet. Also, track account balances and record and balance all economic activity. A G/L (COA) for your business will typically be created by the accountant you hire, but it’s still important to understand, especially in Journal Entries.

You can learn more on this topic by visiting our blog, How to Make a Chart Of Account Specific to Contractors?

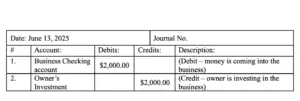

In simpler terms, a continuation of what a journal entry is is a formal record of a financial transaction in a business. It shows what occurred, when, and how it affects the business’s accounts. It’s like a log or note that provides the transaction, which accounts are involved, how much money was moved, and whether the accounts went up (debit) or down (credit). Here is an example below:

- Scenario: You start a small business and deposit $2,000.00 of your money into the business bank account.

The explanation is that the Business Checking Account is an asset, and it’s increasing—debit. Then, the Owner’s Investment represents your contribution to your business—credit. This concept is applied to any G/L or Chat of Account account, such as income transactions—sales receipts, invoices, payments, etc.

What if I have a more complex scenario? And how does software like Quickbooks help?

We will use another example to help you understand complicated scenarios, especially involving more than two accounts being affected. Say you bought office equipment through your business, which was a significant amount, like $5,000. You pay it with cash, but it was $2,000 in cash, and you want to pay the remaining $3,000 later (on credit). This chart is what it would look like:

To explain what happened here, the office equipment is entered as an asset and is increasing – debit the full cost. The cash you used to purchase it is decreasing – credit for the amount you paid upfront. To account for the $3,000.00 that will be paid later (on credit) is a liability and is increasing, so you credit for the balance you still owe.

Of course, there are many other realistic and complex scenarios we can run through, such as those involving sales revenue and sales tax or payroll and payroll deductions. We can say that now you have an in-depth understanding of the basis for a journal entry. Although you might find yourself having too many transactions to handle and other responsibilities your company demands of you, below, we will discuss what Quickbooks can help with to alleviate this.

Let’s continue to discuss Quickbooks and how the software helps prevent you from making manual entries such as the above. So Quickbooks will allow you to take those income transactions, such as customer payments to sales receipts or invoices, or take expense transactions, such as money spent on materials and utilities, and categorize them to the respective account it is affecting. From there, it creates the journal entry and uses the history of similar previous transactions to automate with your supervision, reducing the room for error.

When making these categorizations for transactions and their respective accounts, Quickbooks will enter the journal entry and complete the math of debiting or crediting the affected accounts. If I have you hooked on doing less work and less math involved, look at Quickbooks (hyperlink here) and better understand the software. However, at Waterford Business Solutions, we have advisors to help you choose the best plan that suits you and your company’s size.

Why do I need to use Journal entries? Seems like a hassle.

You might wonder if this can become too much work to keep up with. it’sIt’s crucial to keep organized and accurate financials if you sell your business or if you have to do an insurance audit, bond audit, or any other type of audit. Your company would face financial and legal consequences for not accurately representing the business’s books. Your income statement, balance sheet, and cash flow statement will also be incorrect and lead you to make poor decisions.

For example, buying a new asset on credit creates a liability based on inflated profit you thought you had to cover this liability. You could run into issues with underreporting income to the IRS, which can trigger penalties, or overstating expenses, which is considered tax fraud. Ultimately, you would face serious consequences if you neglect to record accurate journal entries.

Lastly, it’s essential to have your notebook, known as a general ledger or chart of accounts, and to record journals of your day, known as journal entries, for your business, especially for strategizing decisions to grow your business and avoid financial and legal consequences such as tax penalties. Suppose you need more help keeping track of your business notebook, at Waterford Business Solutions. In that case, we have bookkeepers to assist and advisors to advise you on strategies to help you make financial and tax decisions on your business.